Yubico: From Niche Hardware to AI-Era Infrastructure?

This is just an elevator pitch

I’m just a dude on the internet shilling shit stocks. This is not financial advice. We will look into the numbers when Yubico reports its 2025 year-end results on February 12, 2026.

30.1.2026 | YUBICO | SEK 66,50 | 52w high SEK 267,00 | 52w low SEK 66,06

🟢 Trust standard · Recurring revenue · Manufacturing moat · Regulation · Optionality

🔴 Niche · Big tech competition · Transition struggling · Management · “Good enough” threat

What the fuck is Yubico? I was bored at my desk, looked at my keys, saw an old sturdy Yubikey, and checked what was happening with the company. I like the product. Perfect solution (for me). Here’s more: (YouTube link)

I'm here to ramble investment ideas and not teach how to do security, so we ramble. What makes Yubico a good investment candidate? We can DREAM!

This is where the “growth investoors” puke and capitulate, it is beautiful we love this! Business is still the same. “Transition” mode now. Will the subscription model continue to grow? We need to monitor this.

Still solid business.

"Customers buy once, don't return for years" → Subscription

Once you're in with Yubico, you are locked in.

Manufacturing Fortress. Own facilities in Sweden AND USA - no China

Have cash

Profitable, growing, dominant market position…

Worst-case scenario? If growth disappoints… They remain a profitable niche security vendor.

What makes this bet so beautiful is that Yubico has many different paths and narratives it can take. In this clownworld market, narratives are everything. Look at this shit:

Look at this shit: Cloudflare went to toilet and skyrocketed in few days back? “AI AGENTS!” Just one of the examples.

Cloudflare is also a big fan of YubiKeys, and all gigabrains are pretty much fans of this.

Worth noting: "smart people love this product" rarely translates to "good investment." Keep that in mind.

Let’s dream a few Narratives:

AI agents need hardware trust anchors

EU digital ID mandates are coming

Deepfakes make physical auth the only unfakeable layer

From hardware vendor → identity infrastructure

“Prove you’re human” = tap your key

A stupid physical key? That’s the point.

Cloudflare was just a CDN. Palantir was just weird government software. Nvidia made gaming chips. Things get re-rated when the story changes.

What if the stupid YubiKey becomes critical internet infrastructure?

Yubico 90s pitch:

The stock trades like a niche hardware vendor. The opportunity is core identity infrastructure for the AI + digital ID era.

✅ The world is moving from passwords → passkeys → hardware trust

Phishing attacks up 150% yearly over six years

AI now writes better phishing emails than humans do

Attackers using agentic AI to bypass traditional MFA in real-time

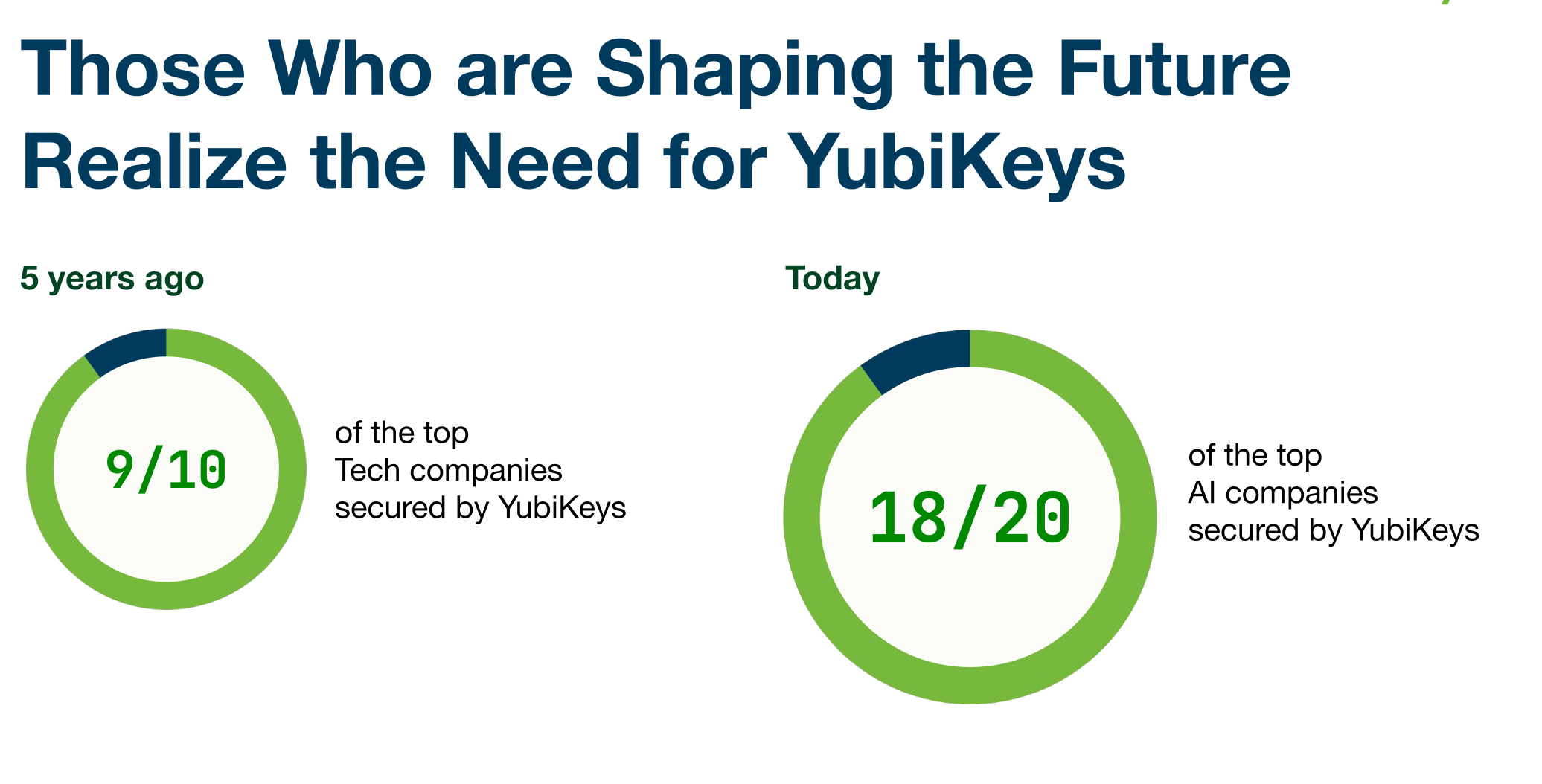

✅ They helped build the standard everyone is adopting

Yubico wasn’t just early—they helped create FIDO/WebAuthn. Third-party validation consistently ranks hardware keys as the highest level of authentication security.

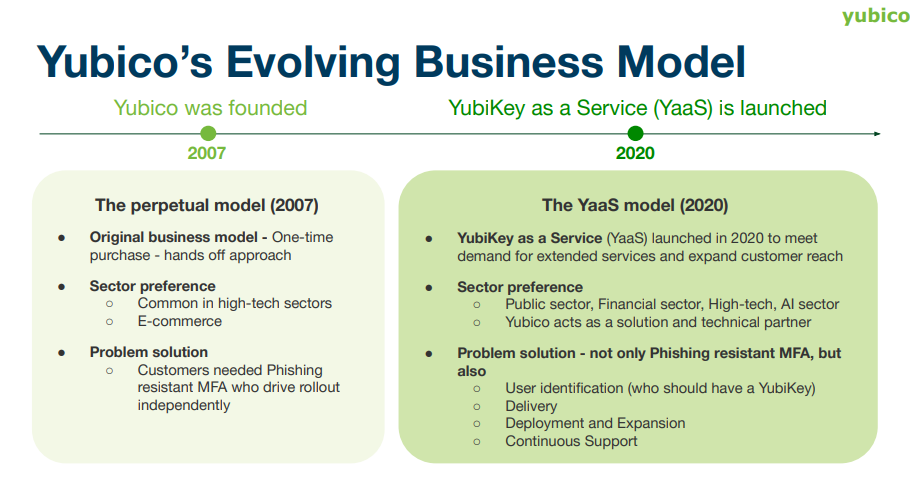

✅ Quietly becoming a recurring revenue story

Keys are “buy once.” But they’re shifting to YubiKey-as-a-Service. Lower cost of entry, value captured over multiple years. The mix is what to watch.

✅ Manufacturing and trust moat

These are security roots of trust, not cheap gadgets. Yubico designs the hardware, firmware, and secure elements. Manufactured in Sweden and the US. Not China.

✅ Optionality is massive

Login security is just the start. Digital identity wallets, EU regulatory push, AI-driven fraud - all increase the value of proving you’re human with a physical credential. If that layer standardizes around passkeys + hardware assurance, Yubico sits at the root.

🚩 Hardware keys remain niche

Best solution, but people choose easy over secure. Software wins by default most of the time.

🚩 Competition is existential

Yubico doesn’t own the identity stack. They’re a small component inside ecosystems controlled by Google, Microsoft, and Apple.

🚩 Subscription transition is struggling

Enterprise sales cycles stretching to 12-18 months. Q3 bookings missed on “delayed large deals.” (Deals are dying). 200+ new hires are burning cash with no immediate revenue impact.

🚩 Management looks lost

New CEO. Consumer strategy is weak. Investor presentations feel like they don’t fully understand their own value prop.

🚩 “Good enough” can be fatal

Apple, Google, and Microsoft are pushing device-synced passkeys - frictionless, free, and baked into phones and laptops. For most users and many enterprises, that’s good enough.

+ Bonus 🚩 Dollar continues to weaken… Currency headwind

Majority of the revenue in Dollars → Reports SEK

Weaknes → More weaknes… Add this currency doomloop to this mix, and we are not even close to the bottom.

At SEK 66, you’re not paying for perfection. You’re buying a profitable business with multiple paths to becoming critical infrastructure for our AI-agent-infested future.

Yubico reports 2025 full-year results February 12, 2026. I’ll be back with the numbers and more bullshit.

This ain’t pretty! :D

Currently at 30,26 SEK (-50% from my elevator pitch).

They just dropped a forced profit warning “inadvertently disclosed.”

Great job! FFS!

Classic move from one of the most hyped company:

Hire aggressively in 2025 → fire people in early 2026.

Very poor job from management.

Bookings down ~25%. WTF?

The business looks shit. The product does not. (I still like it.)

Still: the thesis is not dead yet. None of the kill switches has triggered:

Starts losing money

ARR growth stops (Q1 report is key… doesn’t look great)

They start doing stupid acquisitions

This was a witty gigabrain “mispriced transition story” in early 2026.

Now? Just a painful Swedish small cap to hold.

Update 12.2.2026 | Q4 Results are in. Not pretty. Stock -15% to SEK 55.

The numbers:

🚩 Profitability collapsed - EBIT margin 1.2% vs 17.8% last year. Full year 9.0% vs 18.8%. Ugly.

🚩 Currency doomloop confirmed - Single biggest driver of the ugly headlines.

🚩 Management looks lost - New CEO started December 17th. Give him time...

🚩 Hardware keys remain niche - Top 3 verticals: high-tech, financial services, defense. They're leaning into segments where "good enough" passkeys aren't good enough. Smart, but confirms the niche.

✅ Subscription flywheel is REAL - Strongest confirmation from the report. 28% of bookings now subscription (vs 19% last year). ARR +21% to SEK 391m. Renewals SEK 96m in Q4 alone. Customers are locked in and not leaving!!!

✅ Bookings in constant currency = record quarter. Largest booking quarter in Yubico history when you strip out FX. Demand isn't dying. It's being masked.

✅ Optionality getting real - Straight from the report: "protect user and AI agent identities end-to-end." They're starting to believe their own re-rating story. The market can do what it wants.

✅ Balance sheet is a good - SEK 856m net cash. No real debt. They can fund this transition without diluting you.

Pain isn't over. Transition continues through 2026. This doesn't turnaround in a few quarters. Weakness → More weakness. Currency doomloop still in the mix. We are probably not at the bottom.

Risk/reward? Still beautiful. Thesis holds. We keep dreaming!